VC & Startups

·

6 mins

Prometheus Reimagined: The Entrepreneur's Role in Creating Economic Abundance

The Fallacy of Economic Stasis

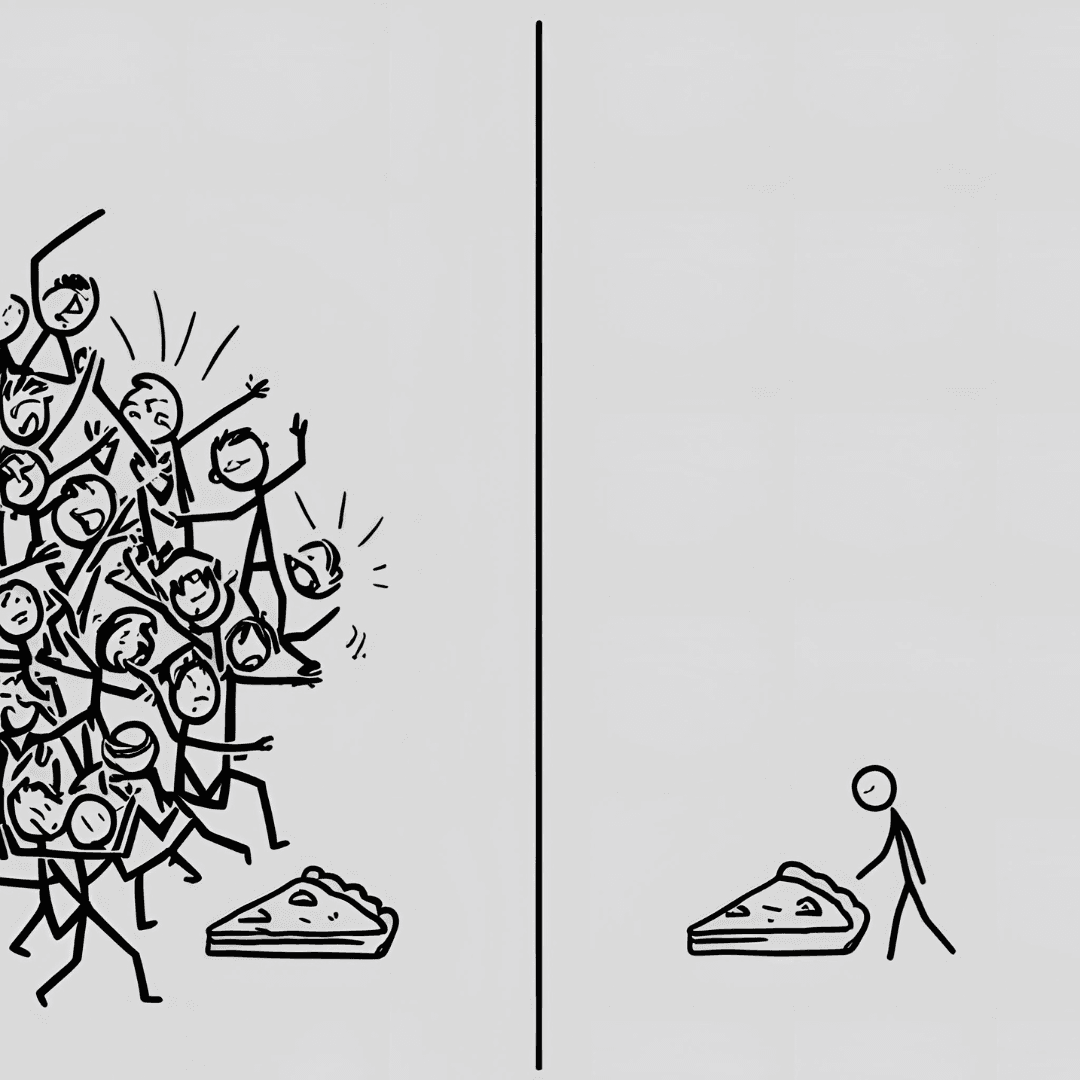

Most people approach economics through the lens of scarcity. They envision the economy as a fixed pie where taking a bigger slice means someone else inevitably gets less. This perspective—deeply rooted in mercantilism and reinforced by zero-sum political rhetoric—fundamentally misunderstands how wealth works. Wealth isn't simply distributed; it's created through a complex interplay of innovation, entrepreneurship, and creative destruction that continuously expands human possibilities.

In one of his 2004 articles, How to Make Wealth, Paul Graham – Co-founder of Y Combinator – extends this idea by describing startups as a way to ‘compress your whole working life into a few years.’ Unlike traditional employment, where value is created incrementally over decades, startups harness leverage and technology to generate wealth rapidly. Just as the venture-backed trading expeditions of the Middle Ages unlocked new sources of value, today’s startups identify and create opportunities where none previously existed. This is not about taking a bigger slice of a static pie but baking entirely new ones.

“Startups are not magic. They don’t change the laws of wealth creation; they just exist at the far end of the curve.” – Paul Graham

Beyond Zero-Sum: The Positive-Sum Reality

The zero-sum fallacy dates back to pre-industrial economic thought, when mercantilists viewed global wealth as fixed and trade as merely shuffling existing resources. This view made sense in a primarily agricultural world with minimal productivity growth. Yet Adam Smith, in his seminal 1776 work "The Wealth of Nations," recognized that specialization and trade could increase total output—a revolutionary insight that challenged the static economic paradigm.

What Smith observed at the dawn of industrialization has accelerated exponentially. Modern economic growth theory, pioneered by Robert Solow and expanded by endogenous growth theorists like Paul Romer, demonstrates that technological innovation—not merely capital accumulation—drives sustainable economic expansion. Romer's crucial insight was that ideas are fundamentally different from physical resources: they're non-rivalrous. When I use your idea, you don't have less of it; instead, we both possess it fully, and society's collective capability expands.

This non-rivalry transforms economics from a zero-sum game to a positive-sum interaction. Global GDP has increased from approximately $1 trillion in 1800 to over $100 trillion today (in comparable dollars)—a hundredfold expansion that would be impossible if we were merely redistributing fixed resources.

Schumpeterian Creative Destruction: The Engine of Renewal

Joseph Schumpeter's concept of "creative destruction" provides a framework for understanding how innovation simultaneously destroys and creates value. The entrepreneur, in Schumpeter's view, is a revolutionary force—disrupting existing market structures by introducing new methods, products, or organizational forms that render existing approaches obsolete.

Consider the transition from horse-drawn carriages to automobiles. This shift displaced established industries—harness makers, stable operators, carriage manufacturers—yet created vastly more value through new industries, increased mobility, and productivity gains. The automobile industry didn't simply redistribute existing wealth; it created entirely new forms of value that previously couldn't exist.

Similarly, digital transformation hasn't merely shifted value from brick-and-mortar retailers to e-commerce platforms. It has created entirely new categories of value—recommendation algorithms, search capabilities, and convenience factors that simply couldn't exist in the physical retail environment. Amazon doesn't merely capture value that once belonged to Sears; it creates new forms of value through capabilities that were previously impossible.

The Knowledge Economy and Increasing Returns

Traditional economics focuses on diminishing returns—the principle that additional inputs eventually yield decreasing marginal outputs. Yet knowledge-based industries often exhibit the opposite: increasing returns to scale. Network effects, where products become more valuable as more people use them, create virtuous cycles of growth that defy conventional economic constraints.

Brian Arthur's pioneering work on increasing returns explains why certain innovations create such explosive value creation. When positive feedback loops dominate—as in social networks, operating systems, or platform businesses—growth becomes self-reinforcing. Each additional user increases the value for all users, creating a multiplicative rather than merely additive effect on total value.

This dynamic explains why digital platforms can scale to billions of users with minimal marginal costs. Facebook's core product costs virtually the same to operate whether it serves one million or three billion users, yet its value increases exponentially with each additional connection. This isn't wealth transfer; it's wealth creation through technological leverage of network effects.

Paul Graham makes a crucial distinction between wealth and money: ‘Wealth is what you want, not money.’ The value created by a successful startup isn’t merely financial—it’s the utility it provides. When a new software platform emerges, it doesn’t merely reallocate dollars; it changes how we interact, work, and think. In a knowledge-based economy, where network effects and increasing returns drive exponential growth, value creation transcends traditional financial metrics. This is why a handful of talented individuals, operating outside conventional structures, can generate outsized impact—something a corporate bureaucracy rarely matches.

Unlike traditional employment, where effort and compensation are loosely correlated, startups create direct leverage between output and reward. This is why ambitious individuals often gravitate toward startups—where returns are tied directly to contribution rather than bureaucracy.

The Philosophical Foundations of Individualism

The economic case for individualism as a driver of wealth creation rests on philosophical foundations articulated by thinkers from John Locke to Ayn Rand. Locke's conception of natural rights and property established the individual as the fundamental economic unit, with the right to own the fruits of their labor. This seemingly simple principle created the incentive structure that would eventually fuel industrial revolution and modern capitalism.

Friedrich Hayek expanded this understanding by recognizing the distributed nature of knowledge in society. In "The Use of Knowledge in Society" (1945), Hayek argued that central planning inevitably fails because no single entity can possess the dispersed, contextual knowledge held by countless individuals. The market's price mechanism allows this distributed knowledge to coordinate economic activity without centralized control—a process that depends on individual agency and local knowledge.

Individualism in this context isn't mere selfishness; it's the recognition that progress emerges from the freedom of individuals to act on their unique knowledge, capabilities, and insights. Innovation requires the cognitive diversity that comes from individuals pursuing distinct paths rather than collectively following predetermined directions.

The Entrepreneutical Method: From Vision to Value

The creation of new wealth follows patterns identified by Israel Kirzner's concept of "entrepreneurial discovery" and expanded by modern theories of entrepreneurial cognition. The entrepreneur, in Kirzner's view, exercises "alertness" to discover opportunities others have missed—gaps between current offerings and potential value that represent untapped potential.

This alertness manifests through what Saras Sarasvathy terms "effectual reasoning"—a distinctly individualistic approach to opportunity. Unlike causal reasoning (selecting means to achieve predetermined ends), effectual reasoning begins with available means and allows goals to emerge through action and discovery. The entrepreneur asks: Given who I am, what I know, and whom I know, what possibilities can I create?

This mindset explains why entrepreneurs often succeed by breaking from conventional wisdom. Steve Jobs didn't conduct market research before creating the iPhone; he envisioned possibilities others couldn't yet articulate. The entrepreneur's individual perspective—their unique combination of knowledge, experience, and vision—becomes the catalyst for creating solutions that wouldn't emerge from collective consensus.

Cumulative Innovation and Standing on Giants' Shoulders

While celebrating individualism, we must recognize that innovation builds cumulatively on previous discoveries. Isaac Newton's observation that he stood "on the shoulders of giants" applies equally to modern entrepreneurship. Today's innovators leverage accumulated knowledge, infrastructure, and technologies created by countless predecessors.

This cumulative nature doesn't diminish individualism but contextualizes it within a broader system of knowledge creation. The entrepreneur combines existing elements in novel ways, adding their individual contribution to the collective knowledge base. Each innovation becomes a platform for future innovations in an ever-expanding cycle of creation.

Open source software exemplifies this dynamic. Individual contributors create specific solutions while simultaneously expanding the commons upon which others can build. Linux, originally one programmer's personal project, has become the foundation for much of modern computing infrastructure through thousands of individual contributions, each solving specific problems while contributing to the whole.

Opportunity Landscapes and First-Mover Advantages

“Brilliant thinking is rare, but courage is in even shorter supply than genius.” – Peter Thiel, Zero to One

Economic opportunity follows identifiable patterns that reward the alertness emphasized by Kirzner. Emerging technologies, social trends, and regulatory changes create what strategic theorists call "opportunity landscapes"—terrains of potential value that aren't immediately obvious to all participants.

Those who recognize these landscapes early gain first-mover advantages, as articulated in Lieberman and Montgomery's seminal work. These advantages include technological leadership, preemption of scarce assets, and switching costs that create customer lock-in. By moving early, entrepreneurs can establish positions that remain advantageous even after others recognize the opportunity.

Consider early cryptocurrency adopters. Those who recognized Bitcoin's potential in 2010-2012 acquired assets at minimal cost that would later represent substantial value. They didn't take this value from others; they recognized potential value before consensus emerged. Similarly, early investors in cloud computing, smartphone applications, or social media didn't merely redistribute existing value—they positioned themselves to capture newly created value as these sectors expanded.

The Democratization of Opportunity

Traditional barriers to entrepreneurship have diminished dramatically through technological advancement. Capital requirements for many ventures have plummeted as cloud computing replaces server infrastructure, digital distribution eliminates physical inventory, and global talent marketplaces provide specialized skills on demand.

Knowledge access has similarly democratized. The MIT OpenCourseWare initiative, launched in 2001, exemplified this shift by making world-class educational content freely available. Today, platforms like Coursera, edX, and YouTube offer instruction from leading experts at minimal or no cost. While formal credentials still matter in certain contexts, the practical knowledge needed to innovate has never been more accessible.

Funding models have likewise evolved beyond traditional gatekeepers. Crowdfunding platforms like Kickstarter and Indiegogo allow entrepreneurs to validate concepts and secure funding directly from users. Alternative financing models including revenue-based financing and community-supported development provide paths to growth without traditional venture capital.

These transformations don't eliminate all advantages of privilege, but they significantly expand who can participate in wealth creation. A programmer in Lagos or Lima can now build and distribute software globally with minimal capital investment, accessing both knowledge and markets that were previously restricted to those in developed economies.

Austrian Economics and Subjective Value

The Austrian school of economics, from Carl Menger to Ludwig von Mises to Murray Rothbard, provides crucial insights into how wealth creation occurs through subjective valuation. In this tradition, value isn't intrinsic to goods or services but exists in the minds of individuals who value them differently based on their unique circumstances, preferences, and knowledge.

This subjective theory of value explains how entrepreneurs create wealth without extracting it from others. By transforming resources into forms that people subjectively value more highly than their previous state, entrepreneurs increase total utility without diminishing anyone else's holdings. The smartphone in your pocket contains minerals that were vastly less valuable in the ground than in their current configuration—a transformation of form that created value rather than transferring it.

This perspective counters the Marxist view that profit necessarily comes from exploitation. When transactions occur voluntarily, both parties benefit based on their subjective valuations. The buyer values the product more than the money exchanged; the seller values the money more than the product. Both emerge subjectively wealthier through voluntary exchange.

Time Preference and Capital Formation

Another Austrian concept—time preference—explains how wealth accumulates through deferred consumption. Those with lower time preference (greater willingness to delay gratification) build capital that enables greater future production. This capacity for delayed gratification represents not extraction but creation through foresight and discipline.

The entrepreneur epitomizes this principle by forgoing immediate consumption to invest in speculative ventures. Jeff Bezos could have enjoyed comfortable consumption after his success at D.E. Shaw, but instead reinvested his capital and labor in Amazon—a venture that required years of delayed gratification before generating returns. This wasn't wealth extraction but wealth creation through the deployment of capital toward future productivity.

The Moral Case for Creative Value

Beyond efficiency arguments, there's a moral dimension to wealth creation versus wealth extraction. Activities that create new value—innovations that solve problems, improve efficiency, or meet unmet needs—have fundamentally different moral standing than those that merely redistribute existing value through force, fraud, or political privilege.

Hernando de Soto's research on property rights in developing economies demonstrates this distinction. When entrepreneurs operate in environments with secure property rights and rule of law, they typically focus on creating value through innovation and service. In environments where property rights are insecure, entrepreneurial energy often diverts toward securing political favor, forming protective cartels, or capturing existing assets—activities that redistribute rather than create wealth.

This insight aligns with public choice theory, which recognizes that rent-seeking—the pursuit of government-granted privileges—diverts resources from productive to redistributive activities. When entrepreneurs succeed through political connections rather than market service, they extract rather than create value, reducing total welfare even as they accumulate personal wealth.

Beyond GDP: Wealth Creation in Quality and Experience

Traditional economic measures like GDP capture only partial aspects of wealth creation. Many innovations create value by improving quality, convenience, or experience in ways that aren't fully reflected in monetary measures.

Consider smartphone applications that provide free services previously unavailable at any price. Google Maps offers navigation capabilities that surpass what was available to professional drivers a generation ago, yet its direct contribution to GDP is minimal. Similarly, access to the world's knowledge through Wikipedia represents massive consumer surplus—value experienced by users far beyond what they pay—that traditional economic measures undercount.

This uncaptured value explains why quality of life has improved more dramatically than income statistics suggest. The average person today, even at modest income levels, can access entertainment, information, communication, and educational resources that were unavailable to the wealthiest individuals a generation ago. This represents real wealth creation that transcends monetary measurement.

Networks and Collaborative Value Creation

While emphasizing individualism, we must recognize that value creation increasingly occurs through collaborative networks. Open innovation, as described by Henry Chesbrough, shows how firms create more value by exchanging knowledge across organizational boundaries than through closed proprietary development.

Individual contributions remain essential within these networks. The GitHub model of open source development exemplifies how individuals, acting on personal motivation and applying specialized knowledge, contribute distinct improvements to collective projects. These networks don't diminish individualism but multiply its impact by connecting complementary capabilities.

Blockchain technologies represent the frontier of this networked individualism. Decentralized autonomous organizations (DAOs) enable cooperation without centralized control, allowing individuals to collaborate in creating value while maintaining sovereignty over their contributions. These structures represent not the abandonment of individualism but its evolution into more complex and powerful forms of voluntary coordination.

Entropy and Value Creation

From a thermodynamic perspective, wealth creation can be understood as the localized reversal of entropy—the creation of order from disorder through the application of intelligence and energy. The entrepreneur organizes resources into configurations that serve human purposes, increasing their utility through purposeful arrangement.

This process is fundamentally creative rather than extractive. The value of a semiconductor chip vastly exceeds the value of the sand from which it derives, not because value was taken from someone else, but because human intelligence organized those silicon atoms into patterns that serve valuable functions. The difference between the value of raw materials and finished products represents wealth created, not wealth transferred.

Conclusion: The Promethean Task

The philosophical and economic foundations of wealth creation converge on a singular insight: prosperity emerges not from capturing existing value but from creating new forms of value through innovation, foresight, and entrepreneurial action. Like Prometheus bringing fire to humanity, the entrepreneur brings forth new possibilities that expand collective capability.

This Promethean task transcends political divisions, offering a path forward that emphasizes expansion rather than division, creation rather than redistribution. By recognizing the positive-sum nature of innovation-driven economies, we shift focus from how to divide existing resources to how to create new solutions.

Individual agency remains the irreplaceable catalyst in this process. Without the entrepreneur's vision, the scientist's curiosity, the investor's foresight, or the builder's determination, the complex systems of innovation that drive prosperity would falter. These individual contributions, while supported by collective infrastructure and knowledge, represent the essential spark that ignites new value creation.

As we navigate economic challenges and opportunities, this distinction between wealth creation and wealth transfer provides a crucial compass. Policies, organizations, and cultural values that enable and celebrate value creation—rewarding innovation, protecting property rights, facilitating voluntary exchange, and supporting entrepreneurial risk-taking—build foundations for sustainable prosperity. Those that focus primarily on redistributing existing resources without expanding capabilities ultimately limit human potential.

The alchemist's mindset asks not "how can I secure my share?" but "how can I transform what exists into something of greater value?" This shift in perspective transforms economic life from a competitive struggle over scarcity into a collaborative adventure of continuous creation—an endless expansion of human capability and flourishing.